This is the second article in our annual series to provide support to you as an entrepreneur that is conducting business in or with America. Although I am not an accountant, CPA or tax attorney, there are certain things that I know (from firsthand experience) about business taxation that I’d like to share with you.

Most small businesses in America are classified as sole-proprietorships, s-corporations, LLCs LLPs or partnerships. If your business falls into one of these categories, then keep reading.

Taxes vs. Tax Return

Although every small business is subject to paying federal income taxes, there are a variety of other taxes (or fees) your company is expected to pay depending on your company’s industry and the state(s) (and often times counties or parishes) in which you conduct business. Such taxes can include:

- sales tax

- mining tax

- utility tax

- communications tax

- various employment taxes

- excise tax

- licensing tax

- annual registration tax

Tax returns consist of a series of forms that must be completed (preferably by a CPA, Accountant or certified tax preparer) based on your company’s financial records for the close of a calendar or fiscal year. As the owner, you must sign the tax returns and ensure they are filed on time. The federal tax return is filed first so that the adjusted gross income can then be reported on all applicable state tax return(s).

2014 Federal Income Tax Return

The 2014 federal tax return deadline is Mar. 16, 2015 as established by the IRS.

There are many forms to complete for your company’s federal income tax return, but the most common are:

- S-Corporation: Form 1120S

- LLC/LLP: Form 8832, Form 1120S or Form 1040 (depending on legal structure)

- Partnership: Form 1065

- Sole Proprietorship: Form 1040

Note that if your company is considered to be a foreign entity, then you will more than likely have to complete and file Form 1120-F. If you hired employees, paid interns, consultants and/or independent contractors during the 2014 calendar year, then you must prepare and distribute W2 and 1099 forms by a certain date BEFORE you can file the federal income tax return.

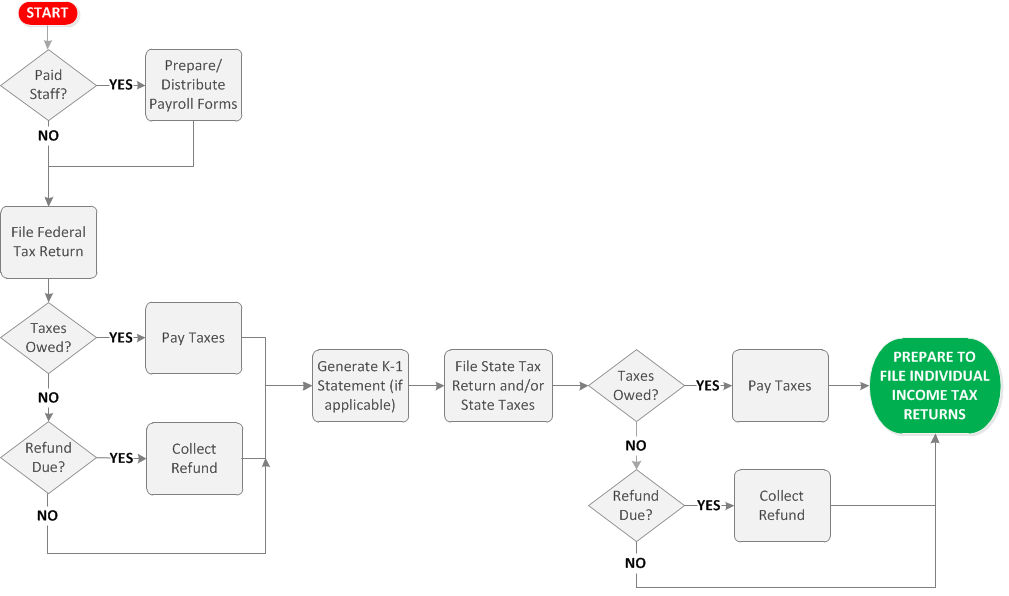

The flowchart below shows the relationship amongst filing employment forms, the federal tax return and state tax return(s):

2014 State Income Tax Returns

The deadline for filing a business state income tax return largely depends on which state(s) you conducted business in. For example, in many states the business tax return is also due on Mar. 16, 2015.

However, in some states the deadline for filing a state tax return for your business is dependent upon whether or not your business operates on a fiscal or calendar year. For example, California and North Dakota require filing based on a time period following the end of your business’ tax year (fiscal or calendar).

Another tricky area for many entrepreneurs is figuring out exactly which state returns must be completed and filed for their businesses. This is why it is SO important that you consult with a CPA, accountant or certified tax preparer to get help in figuring this out.

Depending on the state, you must file a state tax return if your company:

- is registered in a particular state

- conducted business in a particular state

- received business income from/in a particular state (even for online transactions)

- incorporated or formed a partnership in a particular state

So, it is possible that if your business is legally registered in Ohio but you did most of your consulting work in 2014 in Louisiana (and your business received income), you would have to file a state tax return in both Ohio and Louisiana.

To help minimize confusion about this, I’ve compiled a list of each state along with a link to its governing taxation body. If you’re curious about whether or not you will have to file multiple state tax returns, then click on the link corresponding to the state where you conducted business transactions in 2014 to find out.

*Note that South Dakota and Wyoming do not have a corporate/business income tax.

Federal & State Tax Return Filing Preparation Process

Hopefully by now you understand the importance of doing your due diligence in preparing the information necessary to file your company’s federal and state tax returns. It’s also probably no mystery why working with qualified tax professionals is critical to making sure your business stays in legal compliance.

There are certain things you can do throughout your calendar or fiscal year to make the tax return filing process easier and more efficient for the tax professional you work with.

Having a process in place that prevents poor recordkeeping, unnecessary penalties and fines, and chronic filing extensions not only makes the filing process easier for your tax professional but it also ensures a successful audit (should you find yourself in that situation).

Most of us absolutely dread this time of year when we have to file tax returns. Save yourself the agony of going through this experience by: 1) following a well-defined tax preparation process, 2) hiring a tax filing expert, and 3) setting aside some cash reserves in advance just in case you have to pay taxes you weren’t expecting.

Do you have tips you want to share? Please write them in the comments section below!

{kind=link}